Table of Content

You are leaving Discover.com and entering a website operated by a third party. We are providing the link to this website for your convenience, or because we have a relationship with the third party. Discover Bank does not provide the products and services on the website.

You can use a home equity loan for virtually anything, but not every potential use is financially wise. In many cases, people use home equity loans to pay for major home renovations, funding a child's education, or paying off high-interest debts. Taxpayers were able to claim an itemized deduction for interest paid on all home equity loans in tax years up to and including 2017.

A HELOC Won't Change Bad Habits

Home equity loans and home equity lines of credit both use your home’s equity as collateral and carry the same risk of losing your home to foreclosure if you can’t pay them back. A home equity loan has a fixed interest rate, while a HELOC usually has a variable interest rate. Because of this, a home equity loan can be safer than a HELOC if your HELOC has a high balance.

But if you take out a $30,000 HELOC, you'll have the option to only borrow the $25,000 you need. If you're less than thrilled with certain aspects of your home, you may be at a point where you're eager to renovate. And unless you have a giant pile of money sitting in your savings account, you may need to borrow the cash to fund that renovation. From there, you’ll fill out an application through your chosen lender and complete the verification process.

Jobs and Making Money

If you can’t pay back the reverse mortgage in your lifetime, the lender can either foreclose or sue your estate after you pass away. That means even if you leave your home to your kids or grandkids, they may have to sell it to pay off your loan. A home equity loan is a second mortgage that borrows money against the part of your home you’ve already paid for. When you borrow against something, that means the lender can take that thing away from you if you can’t pay back what you owe. Many homeowners have grown their equity significantly in the past year. You can generally borrow up to 80% or 85% of your home’s value with a home equity loan, depending on the lender and your financial profile.

And, if you sell your home, most HELOCs make you pay off your credit line at the same time. If you cancel the contract, the security interest on your home is no longer valid, your home is no longer collateral and can’t be used to pay the lender. The amount that you can borrow — and the interest rate you’ll pay to borrow the money — depend on your income,credit history, and the market value of your home. Many lenders prefer that you borrow no more than80percent of the equityin your home. You use your home as collateral when you borrow money and “secure” the financing with the value of your home. This means if you don’t repay the financing, the lender can take your home as payment for your debt.

Why use a home equity loan for remodeling?

“Homeowners cite a lack of other financing options,” as mortgage rates continue to flirt with 7%. A recent survey found 29% of homeowners are considering tapping into their home equity, noting cash-out refinancing is no longer an option due to high mortgage rates. That's why if you're going to borrow against your home, it might pay to lock in a home equity loan -- quickly. With rates beginning to rise, you may want the security of having a fixed interest rate on the sum you borrow -- and predictable payments to follow. One advantage of taking out a home equity loan over a HELOC is getting to lock in a fixed interest rate on the sum you borrow.

To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. After experiencing homeownership, some people decide it’s not worth it. The time and money involved in maintaining a home can be significant.

Theres A Limit To How Much You Can Borrow

If you only make these minimum payments, you won’t make any progress in paying the principal. Home equity loans can be attractive options if borrowers are seeking a lump sum of cash upfront. With a second mortgage, you might be able to use the equity you’ve accrued to improve your living space and increase your home’s value.

If you don’t already have emergency savings, you may be able to adjust your budget and postpone whatever you need the home equity loan for. If you find yourself in a bind and can’t delay, then a personal loan is an option with cheaper interest rates than a credit card but doesn’t risk your home in the process. But with a home equity loan, the sum you borrow will be subject to a fixed interest rate. That means that your monthly payments under that loan will be predictable and won't change over time. When you borrow with a home equity loan, on the other hand, it’s a one-time infusion of cash that you pay back over time.

Using your home to guarantee a loan comes with some risks, however. The lender may stop credit advances on your account during any period in which interest rates exceed the maximum rate stated in your agreement, depending on what your contract says. Your right to cancel gives you extra time to think about putting your home up as collateral for the financing to help you avoid losing your home to foreclosure. If you have a personal financial emergency, you can waive this right, but be sure that’s what you want before you waive it. If you got money or property from the lender, you can keep it until the lender shows that your home is no longer being used as collateral and returns any money you’ve paid. If the lender doesn’t claim the money or property within 20 days, you can keep it.

The primary consideration when turning your equity into a home improvement is to keep renovation costs within the scope of your project so that they result in an increase in your home’s value. This involves replacing your existing mortgage with one that pays off that mortgage and gives you a little—or a lot of—extra cash besides. Finding the best home equity loan can save you thousands of dollars or more. Different lenders have different loan programs, and fee structures can vary dramatically. Lenders will check your credit and might require a home appraisal to firmly establish the fair market value of your property and the amount of your equity. Several weeks or more can pass before any money is available to you.

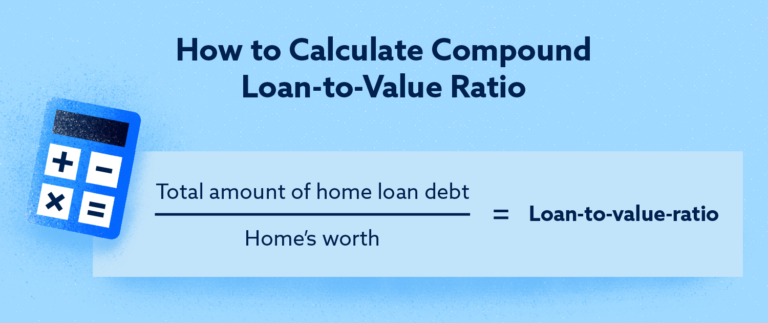

Credit bureaus recommend you keep your revolving balance under 30% of your credit limit. That presented a major problem when HELOCs became popular in the 1990s. HELOCs are classified as a revolving type of credit on most credit reports, the same designation as credit cards. Theres also a limit to the amount you can borrow on a HELOC or home equity loan. To determine how much money youre eligible for, lenders will calculate your loan-to-value ratio, or LTV. Even if you have $300,000 in equity, the majority of lenders will not let you borrow that much money.

The lender can begin to accrue finance charges during the delay period. There’s also a limit to the amount you can borrow on a HELOC or home equity loan. To determine how much money you’re eligible for, lenders will calculate your loan-to-value ratio or LTV. Even if you have $300,000 in equity, most lenders will not let you borrow that much money. Bankrate follows a strict editorial policy, so you can trust that our content is honest and accurate.

That deduction is no longer available as a result of the Tax Cuts and Jobs Act unless you use the money to "buy, build or substantially improve" your home, according to the IRS. Collateral helps, but lenders have to be careful not to lend too much, or they can risk significant losses. It was extremely easy to get approved for first and second mortgages before 2007, but things changed after the housing crisis.

Compare financing offered by banks, savings and loans, credit unions, and mortgage companies. Shopping can help you get better terms and a better deal, which is important when the financing is secured by the value of your home. To pay for this special life event, some couples turn to wedding loans, or personal loans used for weddings. However, the interest rates on these loans are typically higher than interest rates for home equity loans and HELOCs because they are unsecured — not tied to an asset.